Introduction

The significance of investment in the use of a monthly savings plan can not be overstated for any developing economy. One rupee today is worth more than a rupee tomorrow. One way for individuals to increase their income and returns is through investment. Without investment cash flows shrink in the economy thereby slowing economic growth and economic development. High amounts of investment can provide economic stability, better subsections for channels of capital, and ultimately, can create economic growth and opportunities for the increase of income.

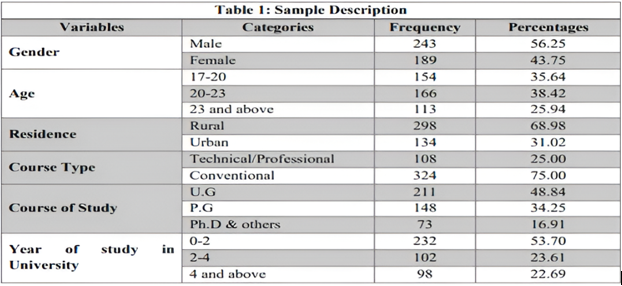

Descriptive Statistics of Factors Influencing Urban Youth Monthly Savings Plan

The variables’ descriptive statistics were acquired in order to comprehend the urban youth landscape. To better understand the landscape of urban youth saving, descriptive statistics for the variables were obtained. The descriptive statistics for each of the dimensions influencing urban youth monthly savings plans have been given in the model of this study. This study had a sample of four hundred urban youth respondents drawn from Nairobi City County.

This study examined gender as a crucial factor that could affect savings. Making sure the data gathered for this study was representative was crucial. A total of 400 participants responded to the survey. 170 were male, or 42%, while 230 were female, or 58%. Therefore, participants in this study were predominantly female.

Analysis

The preliminary analysis of the savings behaviour of students indicated that most students (roughly 53%) were not consistently saving. This implies poor savings behaviour among students. In addition, students’ responses indicated that only one-fifth of sampled students met their monthly savings plan goal. A significant number of students (27%) stated they never met their saving goal.

In relation to ownership of a savings account, most students reported ownership of a savings account; the majority of students would in part attribute their savings account ownership to the government’s focus on financial inclusion. When only 42% of students reported that their quarterly savings balances increased.

Consequently, most students are not able to save consistently and fail to meet savings goals. It is astounding that 72% of students reported it was parents who financially supported them. About 22% of extracted sample data earned income from self-employment or part-time work. These poor savings behaviour patterns of university students can be explained by a low-income level and financial dependency.

Why save?

Savings can serve as insurance, enabling us to navigate these challenges without a doubt. A monthly savings plan provides us with freedom in life. When we save enough money, we can begin making decisions that are dictated by our wants and desires, along with our personal needs, not just our income. Having savings provides a variety of risk opportunities such as starting a business, trying a different job, and becoming a smarter career negotiator without feeling the pressure to earn. Savings also provide a sense of relief by reducing the anxiety associated with unexpected expenses or future planning (such as retirement).

Without a debilitating financial threat looming overhead, we all can feel a little bit of relaxation. Savings can also be invested and, through the wonder of compound interest, turn what may seem to be a nominal amount of money into a sizable amount in the future, especially if we can grow our monthly savings plan faster than inflation, so expensive reality becomes our wealth. Thus, monthly savings plan helps us to select a more confident, independent, and regulated life. Let’s face it. It seems everything in life just keeps getting more and more expensive. Rent increases, tuition never stays the same, and even a trip to the doctor can force us to reach deep into our wallets.

For many of us, by the end of the month, it may feel like all the essentials eat up our entire paycheck. Throw in having to pay off debt like student loans, credit cards, or EMIs, and saving money may feel like a wall goal. Part of the challenge is that many of us weren’t taught the fundamentals of how to manage money. Because of this, it can be easy for us to overspend and not even realize that saving money is diligent work. It may be even harder for us to resist the urge to buy something on impulse with our favourite shops only a click away. Every time we think we are established and saving money.

Conclusion

In conclusion, with many young, lower-income people in urban India who are emerging from a culture of financial insecurity beginning to appreciate the value of saving, it is clear that their journey will not be without hurdles. The challenges of saving due to increasing living expenses, erratic income, debt, and feelings of pressure to spend are daunting. There are some good signs emerging towards better-saving practices, largely energized by access to digital financial tools, along with raised awareness around finances. Overall, we are witnessing a shift towards a generation that is largely asking to be allowed to build a secure, independent future, instead of simply surviving. Given the right support, education, and resources, this group of young people can reshape India’s saving culture, one salary at a time.

FAQs: Building a Smart Monthly Savings Plan for Urban Youth

1. What is a monthly savings plan and why is it important?

A monthly savings plan is a structured approach to budgeting income, reducing unnecessary expenses, and growing financial reserves. It’s especially important for young earners in urban India who face high living costs and financial uncertainty.

2. How do I start a monthly savings plan with a low income?

Starting small is key. Even saving ₹500 a month counts. Track your spending, cut non-essentials, and automate savings. A simple monthly savings plan builds consistency and creates room for growth over time.

3. Can students benefit from a monthly savings plan?

Yes. Students juggling part-time jobs or allowances can benefit from a monthly savings plan by developing habits of budgeting, tracking, and saving for short-term and future goals like gadgets or education.

4. What are the first steps in creating a monthly savings plan?

Begin by listing your income sources and tracking monthly expenses. Then, set aside a fixed percentage for savings. A basic monthly savings plan should also include a target and timeline for your savings.

5. How can a monthly savings plan help me achieve financial goals?

With consistent savings and controlled expenses, your monthly savings plan becomes a roadmap to hit specific targets—like emergency funds, travel, or investments—without falling into debt.

6. What tools or apps support a monthly savings plan in India?

Fintech apps like Groww, Fi, and Paytm Money offer goal-based features that help you stick to your monthly savings plan by tracking progress, automating deposits, and visualizing targets.

7. How does a monthly savings plan help with impulse spending?

A monthly savings plan creates spending boundaries. Allocating funds for essentials and goals naturally limits splurging on unplanned purchases, making you more intentional with money.

8. Should a monthly savings plan include investment strategies?

Yes. Once you have basic savings and an emergency fund, your monthly savings plan can evolve to include SIPs, recurring deposits, or low-risk mutual funds for long-term wealth growth.

9. How do I stay consistent with my monthly savings plan?

Set realistic goals, track your progress monthly, and automate deposits. A visual reminder or app can motivate you to stick to your monthly savings plan even during tight months.

10. What’s a good monthly savings plan for managing student debt?

A tailored monthly savings plan for students should prioritize EMI repayments while still setting aside a small amount regularly. Avoid large non-essential expenses until your debt load decreases.

11. How does budgeting relate to a monthly savings plan?

Budgeting is the backbone of any monthly savings plan. It helps you allocate funds wisely, so you can cover needs, reduce debt, and save consistently without running short.

12. Can a monthly savings plan help improve my credit score?

Yes. A responsible monthly savings plan ensures you always have funds to make timely EMI or credit card payments, which protects or even improves your credit score over time.

13. What are common mistakes in a monthly savings plan?

Underestimating expenses, skipping emergency savings, and setting vague goals can derail your monthly savings plan. Regular reviews and adjustments are necessary to stay on track.

14. Is it ever too late to start a monthly savings plan?

Never. Whether you’re 21 or 31, a monthly savings plan gives you control over your finances. It’s more important to start now than to wait for a “perfect time.”

15. How does a monthly savings plan impact long-term financial health?

A well-executed monthly savings plan builds discipline, reduces reliance on debt, and allows you to take calculated risks—like changing jobs or starting a business—without financial stress.

16. What’s the difference between saving and investing?

Saving typically refers to setting aside money in low-risk places like a bank account, while investing involves using funds to earn returns, often through mutual funds, stocks, or SIPs.

17. Should I pay off debt before I start saving?

Ideally, do both. Allocate a portion of your income to debt repayment and a portion to savings. Prioritizing high-interest debt is crucial, but building an emergency cushion is also important.

18. How can I reduce daily expenses to improve my savings?

Track your daily spending, switch to public transport, cook at home, cancel unused subscriptions, and avoid impulse purchases. These small changes free up cash for your financial goals.

19. Is saving in cash at home a good idea?

It’s not ideal. Cash at home earns no interest and isn’t secure. Instead, use savings accounts or digital wallets that offer security and some return on your deposits.

20. How often should I review my savings and budget?

At least once a month. Regular reviews help ensure you’re on track, adjust for unexpected expenses, and update goals when income or spending patterns change.

21. Can I still save money if I live in a high-cost city?

Yes. It requires more discipline, but by prioritizing essential spending, setting realistic goals, and tracking costs, saving is still achievable even in metros.

22. What role do digital wallets play in managing savings?

Digital wallets can help you segment spending, receive cashback, and keep track of purchases. Some also offer micro-saving features that support financial discipline.

23. How can I make saving a habit and not a burden?

Automate savings, reward yourself for milestones, and keep goals visible. Making saving feel like progress, not punishment, is key to building consistency.

24. What if my income is irregular or freelance based?

Create a flexible budget with a low baseline and save more during high-income months. Emergency funds are even more critical when income is unpredictable.

25. Is it okay to pause saving during a financial emergency?

Yes, during genuine emergencies, it’s okay to redirect funds. However, once stability returns, rebuilding your safety net should become a top priority.

Penned by Priyanshi Chaudhary

Edited by Somewrit Sekhar Maiti, Research Analyst

For any feedback mail us at info@eveconsultancy.in

Finance made simple, fast, and fun! 🏦💡 Sign up for your daily dose of financial insights delivered in plain English. In just 5 minutes, you’ll be smarter already!

Simplify Your Business Compliance with Eve Consultancy

Eve Consultancy is your trusted partner for end-to-end compliance services, including Company Incorporation, GST Registration, Income Tax Filing, MSME Registration, and more. With a quick and hassle-free process, expert guidance, and affordable pricing, we help businesses stay compliant while they focus on growth. Backed by experienced professionals, we ensure smooth handling of all your legal and financial requirements. WhatsApp us today at +91 9711469884 to get started.

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.