Forensic Accounting

The American Institute of Certified Public Accountants defined forensic accounting as the application of certified public accountants’ (CPAs’) specialized knowledge and investigative skills to collect, analyze, and evaluate evidential matter, as well as interpret and communicate findings in a courtroom, boardroom, or other legal or administrative venue. The scope of forensic accounting is not limited to investigation, but it covers various services that a typical forensic auditor will not provide, like financial fraud detection and prevention, providing legitimate support, corporate governance and regulatory compliance, and dispute resolution. There are various financial fraud detection techniques that the institute employs to identify and mitigate fraud risks. These may include machine learning algorithms, anomaly detection, and behaviour analysis. Financial fraud, particularly in the banking sector, is a threat to the global economy, trust of financial institutions, and individuals, like the 2008 financial crisis, which happened due to banking scams. According to the UK Finance 2022 report, billions are lost due to fraudulent activities, highlighting the need for a strong AI-powered financial fraud detection model.

Forensic Accounting Techniques

Traditional ways

- Scrutinise financial accounting statements (balance sheet, cash flow, and profit and loss statement) of many years to find the pattern in these reports to detect any abnormality in these statements.

- Monitoring the trail of financial forensic accounting transactions to ascertain the sequence of events to uncover complex financial webs to identify embezzlement, money laundering, and illicit financial activities.

- Interviews and interrogations are an old traditional technique of gathering evidence regarding fraudulent activities within an organization.

- Reviewing and analyzing all documents that are attached to financial forensic accounting statements for cross-examination to detect subtle traces that will be useful in court.

Digital Forensic Accounting Techniques

We have seen a paradigm shift in the forensic accounting system; as a result, modern-day frauds are more sophisticated, involving offshore assets, complex financial instruments, and digital assets, so forensic accountants need to upgrade their skill set to cybersecurity.

- Data Mining: Accountants utilize data mining to identify anomalies in financial transactions that would otherwise go undetected in typical manual processes.

- Statistical analysis and predictive modeling: help in identifying areas susceptible to fraud and strengthening fraud prevention measures.

- Machine learning and blockchain technology: It analyses large datasets and identifies fraud patterns, while blockchain decentralizes ledgers for transparency and integrity.

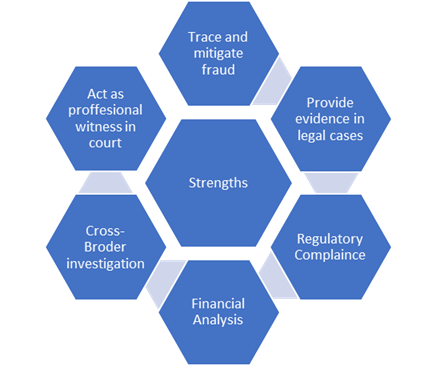

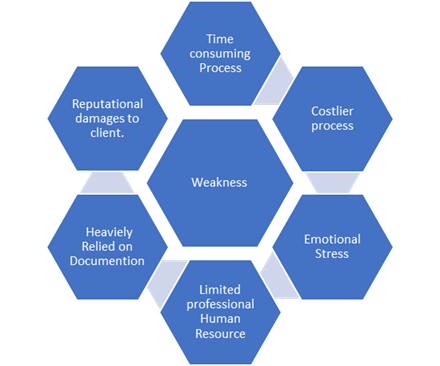

SWOT Analysis of Forensic Accounting

Challenges to Forensic Accounting

Sophisticated Fraud: It is difficult to detect and catch fraudsters, as criminals are using cryptocurrency , encryption tools and other digital advanced tools to scam.

Legal Implications: When accountants propose their evidence in court, it may get opposed as different experts interpret financial data differently.

Tough Market Competition: As the number of forensic accountant firms is growing, it may affect firms, profitability and fees, especially small firms, due to which the quality of their service can get influenced.

Security Risks: As these firms deal with the internal data of a company, any leakage of sensitive information may cause legal obligations.

Pressure from powerful clients: Sometimes, results are not accurate as firms get pressured by high-profile clients to mislead the evidence to reduce financial charges.

Growth Prospect in Forensic Accounting

Cross-Border Investigation: Due to technological advancement, now firms can expand their business across the world as international forensic accountants will have more authenticity in high-profile cases.

Rising in corporate fraud: As the number of financial crimes is increasing, so are forensic accountants required for investigation.

Data Analysis and Forensic Technology: The data analytic tools are helping in finding hidden patterns leading to fraud, increasing the efficiency of forensic accountants.

Increased Regulation: In order to comply with financial regulation, companies are hiring accountants to prevent legal obligation.

ESG audits: ESG (Environmental, Social, and Governance) is an important factor for the company stakeholders nowadays, so forensic accountants can verify ESG reports, as many companies falsify their reports to maintain a good image.

Conclusion

Forensic accountants need to integrate digital techniques with human intelligence, as criminals have found sophisticate ways to do illegal activities. In place of traditional methods that mainly rely on manual auditing and sampling techniques, accountants use digital methods, such as AI-powered tools for real-time fraud detection, Therefore, technological advancements have greatly improved the efficiency of the financial fraud detection process by saving time and resources for forensic investigation. Concerns about data privacy, algorithmic bias, and the requirement for human expertise in complex fraud cases are some of the difficulties that accountants encounter when utilising these AI tools in the financial fraud detection process. Two difficult aspects of the financial fraud detection process are transparency and adherence to data privacy laws.

References

FAQ : Forensic Accounting

Q1: What is forensic accounting?

Forensic accounting is a specialized area of accounting that involves investigating financial records for fraud, embezzlement, or legal disputes.

Q2: How does forensic accounting differ from regular accounting?

Unlike traditional accounting, forensic accounting focuses on examining financial data for legal evidence in cases like fraud or litigation.

Q3: Who needs forensic accounting services?

Businesses, law firms, government agencies, and insurance companies use forensic accounting to uncover financial irregularities.

Q4: What are common types of forensic accounting cases?

Common cases include corporate fraud, employee theft, insurance claims, bankruptcy, and divorce settlements.

Q5: When should a company consider forensic accounting?

A company should consider forensic accounting when it suspects fraud, faces a financial dispute, or needs evidence for legal proceedings.

Q6: What skills do forensic accounting professionals need?

Professionals in forensic accounting need strong analytical skills, attention to detail, legal knowledge, and expertise in financial auditing.

Q7: How does forensic accounting help in fraud detection?

Forensic accounting helps detect fraud by identifying unusual patterns, hidden transactions, and inconsistencies in financial statements.

Q8: Can forensic accounting be used in court cases?

Yes, forensic accounting is often used as legal evidence in court, and forensic accountants may testify as expert witnesses.

Q9: Is forensic accounting only used for big companies?

No, forensic accounting is used by both large and small businesses, especially when financial misconduct is suspected.

Q10: What tools are used in forensic accounting investigations?

Tools like data analysis software, audit trails, and accounting platforms help streamline forensic accounting processes.

Q11: How long does a forensic accounting investigation take?

The length varies depending on case complexity, but most forensic accounting investigations take a few weeks to several months.

Q12: Can forensic accounting uncover money laundering?

Yes, forensic accounting is a critical tool in tracing money laundering and other financial crimes through detailed analysis.

Q13: What is the role of forensic accounting in divorce cases?

In divorce cases, forensic accounting can help uncover hidden assets, verify income, and ensure fair financial settlements.

Q14: Do insurance companies use forensic accounting?

Yes, forensic accounting helps insurance companies assess fraudulent claims and determine financial losses accurately.

Q15: Is forensic accounting a growing career field?

Absolutely. With rising financial crimes, the demand for forensic accounting professionals is growing in both public and private sectors.

Penned by Manshika

Edited by Sneha Seth, Research Analyst

For any feedback mail us at info@eveconsultancy.in

Finance made simple, fast, and fun! 🏦💡 Sign up for your daily dose of financial insights delivered in plain English. In just 5 minutes, you’ll be smarter already!

Simplify Your Business Compliance with Eve Consultancy

Eve Consultancy is your trusted partner for end-to-end compliance services, including Company Incorporation, GST Registration, Income Tax Filing, MSME Registration, and more. With a quick and hassle-free process, expert guidance, and affordable pricing, we help businesses stay compliant while they focus on growth. Backed by experienced professionals, we ensure smooth handling of all your legal and financial requirements. WhatsApp us today at +91 9711469884 to get started.